Citibank paid $29.5 million to settle TCPA claims in 2023. One automated dialing campaign. Wrong consent documentation. For financial services firms looking at AI calling, compliance isn't optional. It's the first question you have to answer. And it got harder after February 2024.

The FCC's 2024 ruling confirmed that AI calling financial services compliance falls under TCPA, covering AI-generated voices specifically. That ruling changed the calculus for every mortgage lender, loan servicer, and debt collector running outbound calling programs. Is AI cold calling legal in financial services? Yes, with the right consent framework in place.

This guide covers TCPA consent tiers, FDCPA requirements for collections, disclosure scripts that pass audit, loan officer follow-up workflows that scale without legal exposure, and the cases where AI calling doesn't belong.

What the FCC's 2024 Ruling Changed

For years, some firms operated AI calling under the assumption that synthesized voices occupied a gray area. They don't anymore. In February 2024, the FCC ruled that AI-generated voices used for calling fall under TCPA, subject to the same requirements as autodialed calls with prerecorded messages.

TCPA penalties run $500 to $1,500 per call. For a mortgage servicer running thousands of outbound follow-up calls monthly, a single non-compliant campaign doesn't just create legal exposure. It creates existential financial risk. Our TCPA compliance guide for AI calls covers the full regulatory breakdown.

Three things shifted with the 2024 ruling:

- AI-generated voices now require the same consent tier as robocalls to cell phones

- The FCC's 'human impersonation' test no longer determines TCPA coverage

- State mini-TCPA laws in California, Florida, and Texas now apply more clearly to AI calling platforms

TCPA Consent Tiers for Financial Services AI Calling

TCPA has three consent tiers. Which one you need depends on the channel, the message type, and whether you're calling a cell phone or landline.

Prior Express Written Consent

Prior express written consent (PEWC) is required for autodialed or prerecorded calls to cell phones for marketing or solicitation. For most financial services AI calling campaigns, PEWC is the bar you need to hit. The consent has to be in writing, name the specific calling company, and include explicit agreement to receive autodialed calls. Vague language fails.

Prior Express Consent

Prior express consent covers autodialed calls that aren't for marketing purposes. Loan servicer payment reminders to existing customers sometimes qualify here, but the line between 'informational' and 'marketing' is contested. Regulators have moved it before. Don't bank on the lower tier for outbound lead follow-up campaigns.

The established business relationship (EBR) exemption is largely dead for cell phone calls under current TCPA. Don't rely on it. For loan officers running follow-up on new leads, PEWC is almost always required. Get it at the point of lead capture: on the website form, in the loan application intake flow, or via text opt-in confirmation.

FDCPA Rules for AI Debt Collection Calls

If you're in collections or loan servicing with delinquent accounts, FDCPA adds another layer on top of TCPA. The Fair Debt Collection Practices Act doesn't care what technology places the call. It governs the content and timing regardless.

- Mini-Miranda disclosure required in every call: “This is an attempt to collect a debt. Any information obtained will be used for that purpose.”

- No calls before 8am or after 9pm in the consumer's local timezone

- Maximum 7 calls per week to the same consumer under CFPB's 2021 rule

- Immediate opt-out mechanism: a single keypress or spoken command must stop future calls

AI voice agents handle some of these requirements better than human agents. The Mini-Miranda never gets skipped when it's baked into the script. Call timing is enforced at the system level. The 7-call weekly limit is tracked automatically rather than manually calculated across a collections team.

Where AI collections calling breaks down is nuance. A consumer who says 'my spouse died last month and I'm dealing with estate issues' needs a human. Build escalation triggers for those conversations. That's not a failure of AI. It's the right design.

Consent Templates and Disclosure Scripts

Written consent forms are only as good as their specificity. The FCC has invalidated blanket consent forms that didn't name the calling entity or specify autodialing. Vague language creates the illusion of protection without the substance.

A compliant PEWC form needs all of the following:

- The name of the specific company placing calls, not just the brand umbrella

- A statement that calls may be placed using automated technology, including AI-generated voices

- The phone number or numbers the consumer is consenting to receive calls at

- Voluntary agreement language with no forced consent tied to service eligibility

California AB 302 (effective July 2024) adds an AI identity disclosure requirement. If a consumer directly asks whether they're speaking to an AI, the system must say yes. Other states are moving in the same direction. Building that disclosure into every call opener is the safer approach regardless of where your leads are located.

A call opener that passes compliance review in most jurisdictions:

Hi, this is [Name] calling on behalf of [Company] about your home loan application. I'm an AI assistant. This call may be recorded for quality and compliance purposes. If you'd like to be removed from our call list, just say 'stop' at any time.

Loan Officer Follow-Up: Compliant AI Workflows at Scale

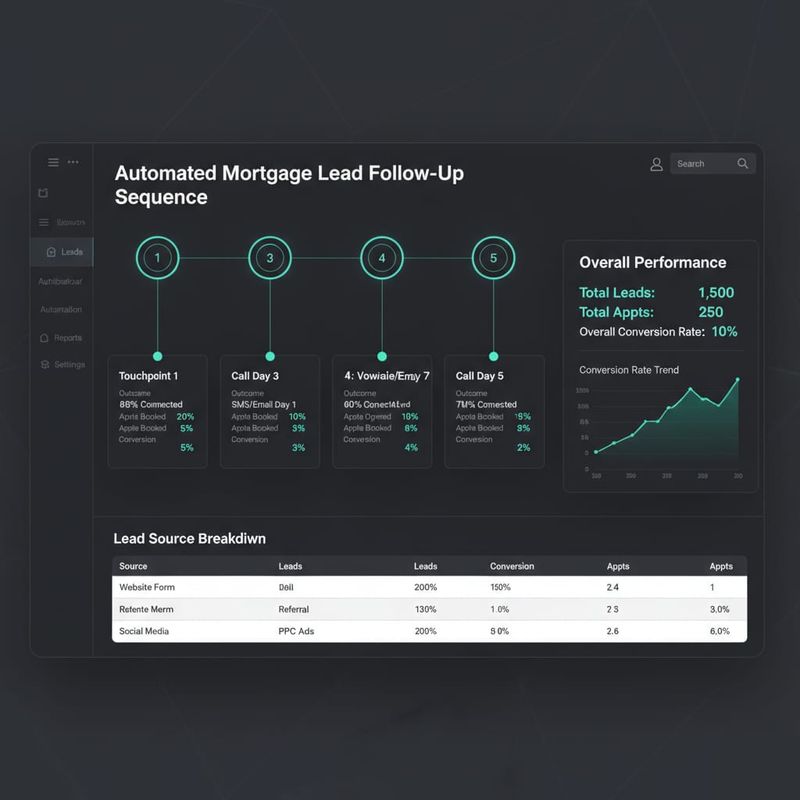

Mortgage lead follow-up is where AI calling delivers the biggest return in financial services. 80% of deals need five or more touchpoints. A loan officer with 50 active leads can't manually make 250 calls. Follow-up automation solves the volume problem without adding headcount, and it can run within the TCPA consent framework you've already established at lead capture.

- Day 0, within 5 minutes of form submission: Speed-to-lead call. Short, informational. Confirm interest, offer to schedule a consultation. This is the call that books meetings.

- Day 2: Reminder call. Still here to help, with a specific time-sensitive offer if applicable.

- Day 5: Value-add call. A current rate snapshot or market update relevant to their inquiry.

- Day 10: Re-engagement call. Changed circumstances check.

- Day 21: Final outreach. Soft close with an easy opt-out.

Each call in this sequence uses the same PEWC obtained at lead capture. No additional consent needed for follow-up calls to the same number. But if the lead asks to stop at any point, that instruction has to propagate to all future calls immediately. No 'we'll update our system in 48 hours.'

Smart Campaigns handles this at scale: timezone-aware scheduling, automatic DNC honoring, and retry logic that distinguishes a busy signal from a declined call. The platform processes 63,000+ AI calls daily, which means the compliance machinery has been tested across real financial services deployments.

AI Call Recording and Audit Trail Requirements

Every financial services AI calling deployment needs an audit trail. Not just for TCPA defense. CFPB, OCC, and state banking regulators now scrutinize call programs during examinations. An audit trail that's a year old and incomplete is worse than no audit trail at all.

The audit trail needs to capture:

- Consent record: who consented, when, to what, and from which form or channel

- Every call attempt: timestamp, number called, duration, outcome

- Full call recording and transcript for every completed call

- Opt-out requests and the exact timestamp they were processed

- Consumer complaints and resolution steps with dates

100% call recording and transcription gets you most of the way there. The piece most firms miss is consent provenance: linking the call record back to the original opt-in record. Build that link in your CRM at lead creation, not retroactively. A CRM that stores PEWC timestamps and call history in the same contact record is your primary audit exhibit.

For DNC compliance at volume, do-not-call list management for AI dialers can't run on manual processes. Every lead uploaded to a campaign should run against federal and state DNC registries before the first call. Scrubbing after the fact isn't compliance.

Where AI Calling Doesn't Fit in Financial Services

Compliance aside, not every financial services call belongs in an AI queue.

Complex loan modification discussions, hardship accommodations, and bankruptcy-adjacent conversations need humans. The regulatory exposure of a mishandled sensitive conversation outweighs any efficiency gain. Regulation X servicing rules for borrowers in distress have specific requirements a scripted AI agent can't reliably satisfy.

Calls involving disputed debt under FDCPA are also risky territory for AI. Cease-and-desist invocations, dispute processes, and verification requests have too many conditional paths. Route those to licensed representatives.

Where AI calling does work in financial services:

- New mortgage lead follow-up (rate-sensitive, time-critical, PEWC captured at lead form)

- Loan application status updates for existing applicants

- Pre-approval appointment setting with direct calendar booking

- Annual review scheduling for wealth management clients

- Payment reminder calls on accounts in good standing

The ROI calculator can show you the dollar difference between your current manual follow-up rates and AI-assisted outbound across your specific lead volume.

Compliance isn't a reason to avoid AI calling in financial services. It's a design requirement. Get the consent right at lead capture, build the disclosure into every script, maintain the audit trail, and route the hard cases to humans. That's it.

If you want to see what a compliant AI calling deployment looks like for your specific loan origination or servicing workflow, book a strategy call. We can have you live in two weeks.

Frequently Asked Questions

Get AI calling tips in your inbox

No spam. One email per week with actionable sales automation tips.